Chime – Mobile Banking

com.onedebit.chime

Safety

Safety

Advertisement

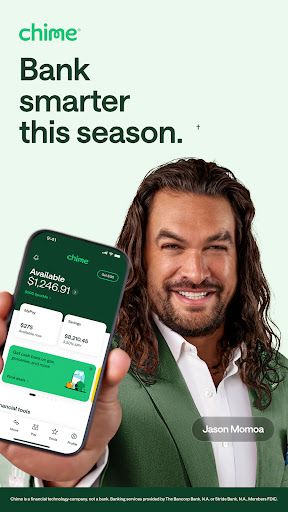

Chime positions itself less like a traditional bank account and more like a streamlined financial toolkit for people who want faster access to income, fewer routine fees, and better day-to-day money control. That pitch lands well. From checking and savings to credit building and overdraft coverage, the app is clearly designed around practical financial friction points rather than flashy extras. The result is a service that feels modern, utility-driven, and especially appealing to users who are tired of monthly maintenance charges and delayed pay cycles.

The strongest part of the Chime experience is how directly it addresses cash flow. Early access to pay through qualifying direct deposit is a genuinely useful feature, and the optional MyPay line adds another layer of flexibility for users who occasionally need short-term breathing room. SpotMe also gives Chime an edge, offering fee-free overdraft coverage on eligible transactions and ATM withdrawals for qualified users. In real-world terms, that makes the app feel more forgiving than many legacy banking products, which still rely heavily on punitive fee structures.

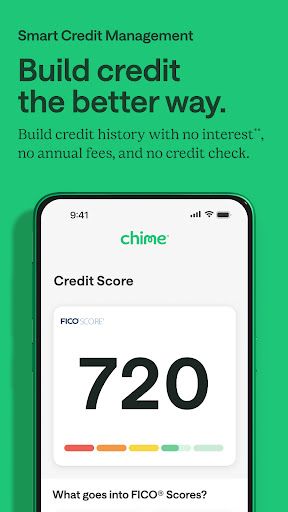

Chime also performs well as a financial habit builder. The automatic savings tools are intuitive and easy to live with, helping small transfers happen in the background rather than requiring constant manual effort. The high-yield savings component adds meaningful upside, though the best APY is tied to eligibility requirements that not every user will maintain. On the credit side, Chime's secured credit card setup is one of its more compelling long-term features. It turns everyday spending into a structured path toward building or maintaining credit, and that focus on accessible credit management gives the platform broader value than a basic spending account alone.

From a UX perspective, Chime feels polished and accessible. The app emphasizes clarity over complexity, and its core tools are laid out in a way that makes routine tasks feel quick rather than intimidating. Security features and 24/7 live support strengthen the experience, especially for users who want reassurance beyond self-service help articles. That said, Chime is not without trade-offs. It is a fintech platform rather than a traditional bank, and some features depend on eligibility, network access, or partner-bank terms. Out-of-network ATM fees, variable savings yields, and limits on overdraft or early pay access mean the headline benefits may not look identical for every customer.

Overall, Chime is a robust and highly practical finance app that succeeds by making common money tasks less painful. Its best features are not gimmicks, they are solutions to real consumer frustrations: waiting for payday, getting hit with small but frequent fees, and struggling to build savings or credit consistently. While the fine print matters, the core product is intuitive, competitive, and genuinely useful. For users who want a more flexible, mobile-first alternative to traditional banking, Chime is an impressive option with clear everyday value.

Comments